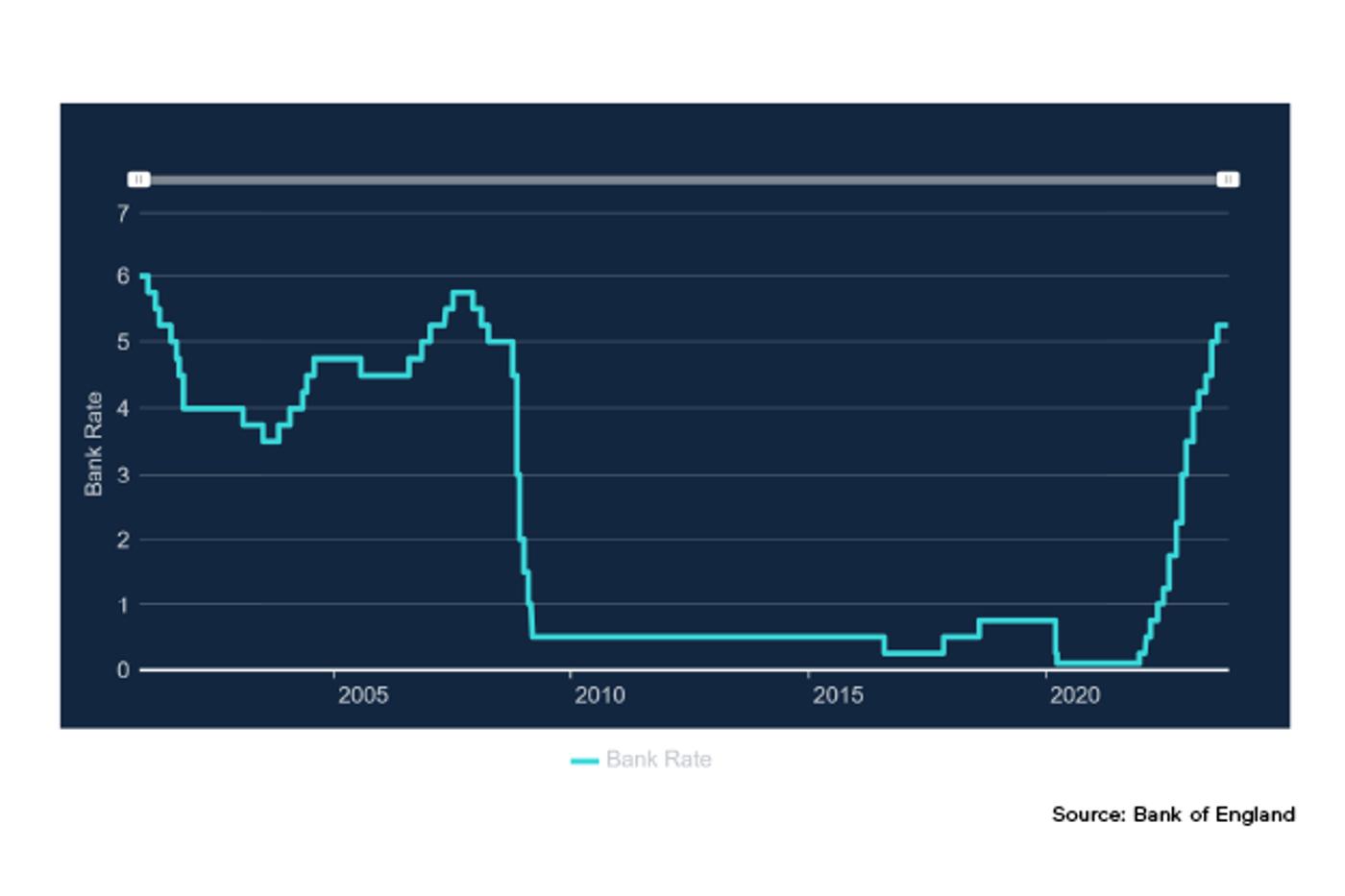

For nearly 15 years, since the Great Financial Crisis (GFC) of 2008, interest rates were historically low. Great if you were a borrower, not so much if you had money on deposit with a bank or building society.

Since December 2021, the Bank of England Base Rate has risen from 0.1% to 5.25%, nearly back to pre-GFC levels. Those of us with savings are enjoying the fact that we’re getting meaningful interest payments every month or every year, even while those renewing their mortgage deal are feeling a great deal of pain.

With interest rates back at reasonable levels, does it make sense to hold more money on deposit?

The real enemy: Inflation

To answer that question, we need to think about our reasons for investing. Quite simply, we invest money so that we can spend it later. We pay into a pension so we can draw it down when we retire. We save for next year’s holiday so that we don’t have to borrow the money to pay for it next year.

The problem with spending money in the future is that its buying power is being continually eroded by inflation. If a holiday costs us £1,000 now, it’s going to cost us £1,500 in ten years, for example. So, we need to invest in such a way as to beat inflation.

We live in interesting times

As I write in late 2023, we are living through an unusual (though not unprecedented) period of history. In the last five years we’ve had a global pandemic, our departure from the EU and war in Europe.

As the world emerged from lockdown, demand soared and supply couldn’t keep up. The war in Ukraine has affected energy and food supplies and countless other commodities. It’s more difficult for the UK to do business in Europe now. All of these factors have driven inflation sky-high and only now is it starting to reduce, though not as quickly as the PM and Chancellor would like.

To battle inflation, central banks raise interest rates. I think we’re heading for an unusual situation where, for a time, interest rates will be above inflation. This means that it is possible to actually make money by keeping money in the bank on deposit.

Deposit = short-term. Investing = long-term

This is, as I say, an unusual situation and it won’t last long. In a normal state of affairs, interest rates stay at or below the prevailing rate of inflation. The Bank of England wants to make sure that inflation is coming down consistently so they’ll hold interest rates up for a while, but they will start to bring them down before too long.

In normal times, you can’t beat inflation by keeping money on deposit and that’s why you only hold cash in the bank for short-term spending or for an emergency fund that you know will be there when you need it.

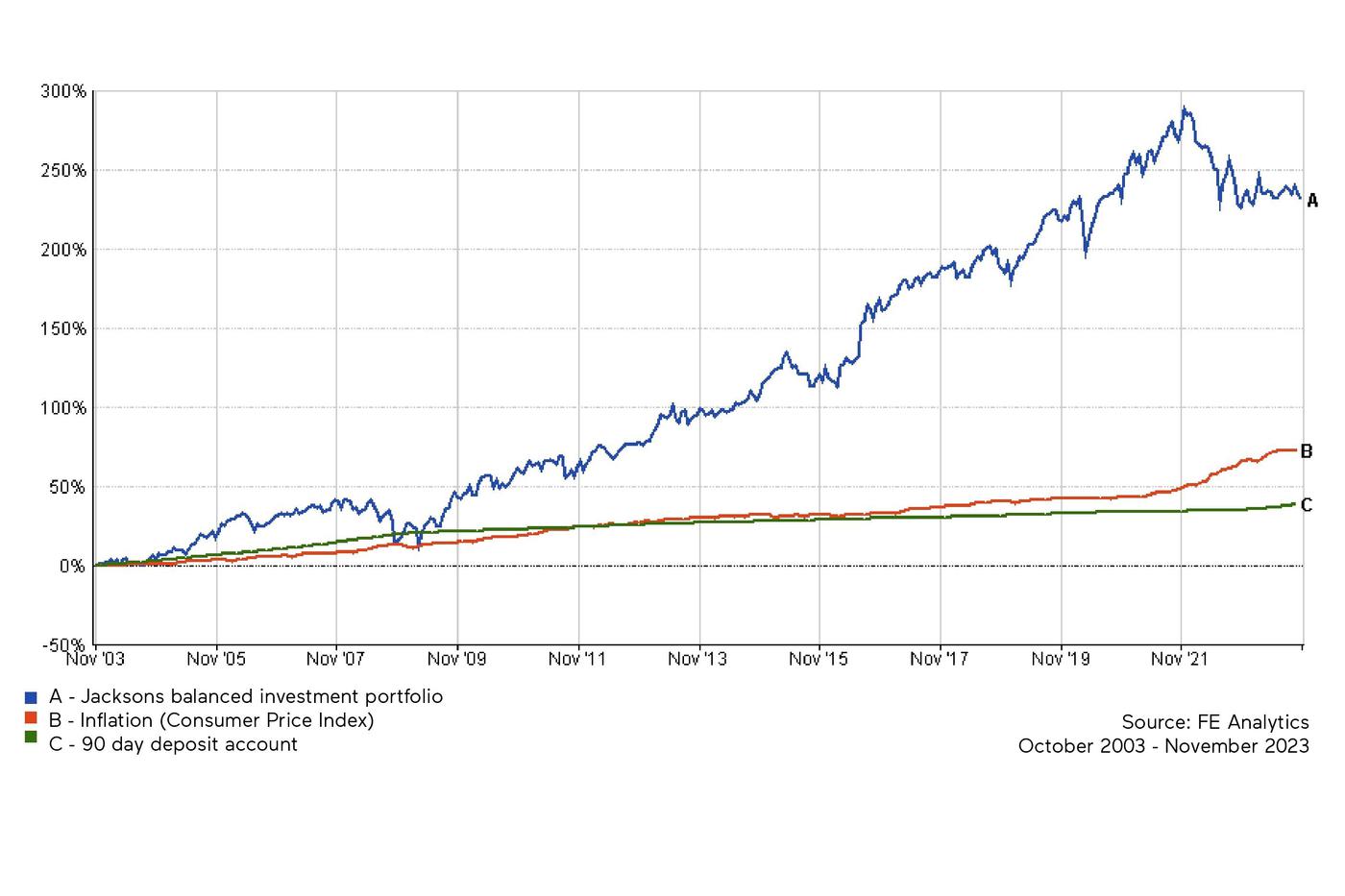

For any longer-term savings, where we need to beat inflation, the only option is to invest.

History shows us that only real assets like shares, bonds, commodities and property will beat inflation, and then only given enough time. In the short term, those investments can fall in value.

It’s that short-term volatility that makes the relative safety of deposits so attractive. But that safety comes at the expense of us beating inflation.

And so, we have to choose our poison, somewhat. We either lose to inflation, but see our balances stay the same, or we watch our investment balances rise and fall, but at least we know we’ll beat inflation given long enough.

Conclusion

And so much depends on our tolerance for volatility and our understanding of risk.

If we would lose sleep worrying about the balance of our investments falling, then we might favour keeping our money on deposit.

If we understand that inflation is the real enemy and can do far more damage to our wealth over the long term, then we might be able to live with short-term volatility in order to remove that possibility.

I think that while interest rates remain high, there is an argument for holding a little more in cash than we might ordinarily do.

But we should not take money out of a volatile market and hold it on deposit ‘until things settle down,’ because they will never settle down! Volatility is the price of entry for investors. We just need to ride it out for the long term.

Nothing has really changed, despite the strangeness of the times we live in. Cash deposits are for the short term, and for long-term money, we should be investing.